How Does My Business Credit Card Impact My Personal Credit Score?

If you’re a small business owner, you probably understand the significance of maintaining good credit. But did you know that your business credit card can

When you’re on the hunt for a new home, understanding the various financing options available can make a significant difference

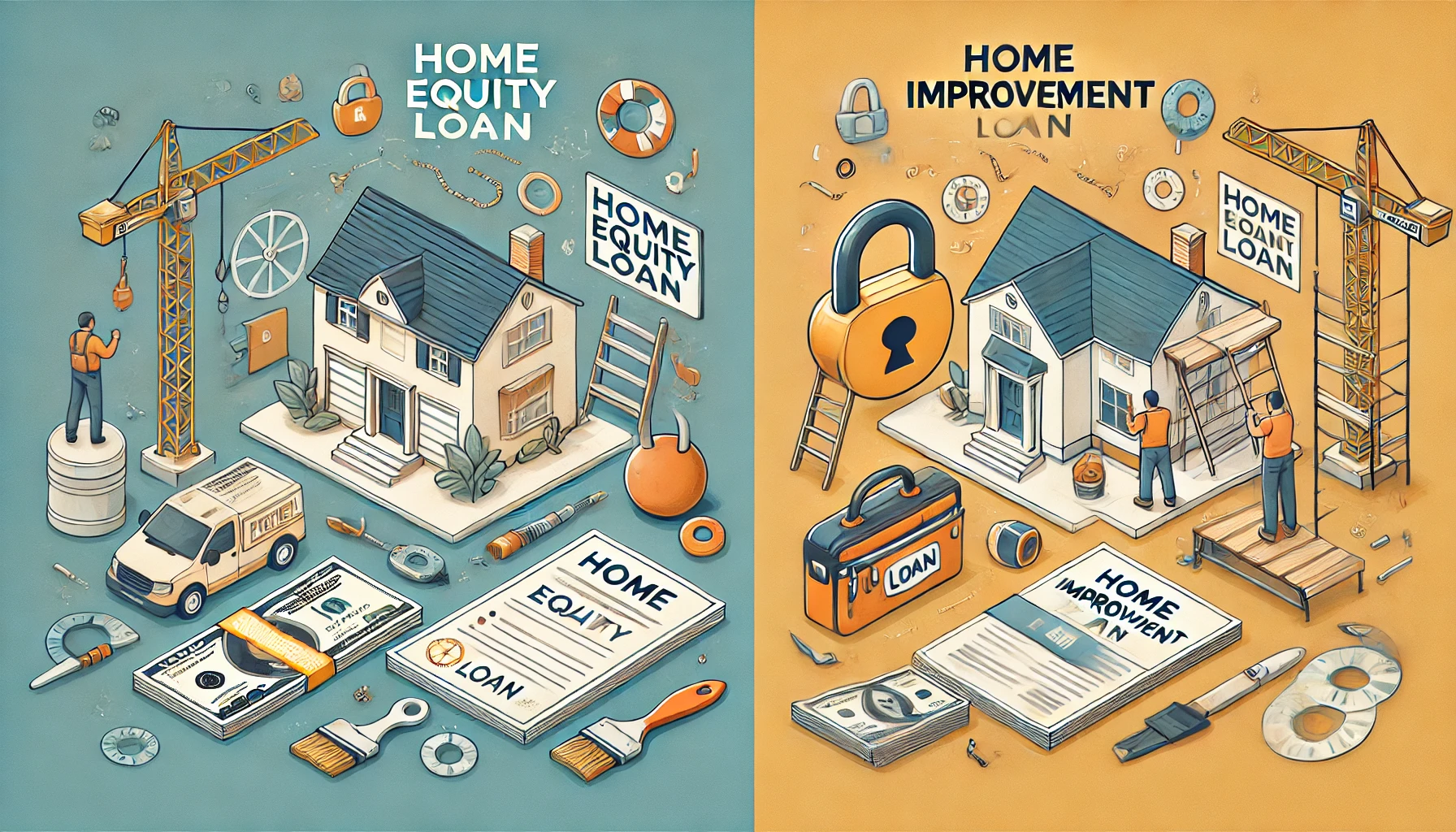

Homeowners often find themselves needing extra funds for various reasons, from remodeling kitchens to consolidating debts. Two popular options are

Life can throw curveballs when we least expect it. Whether it’s an unexpected medical bill, car repair, or another sudden

Car insurance is essential for protecting yourself and others on the road. With various types of coverage available, it can